Insights

Core Equity: Staying the Course on Long Term Secular Growth

- Continue to focus on high-quality companies.

- Balanced exposure between cyclical and defensive sectors.

- Positioning toward AI mega trend and beneficiaries.

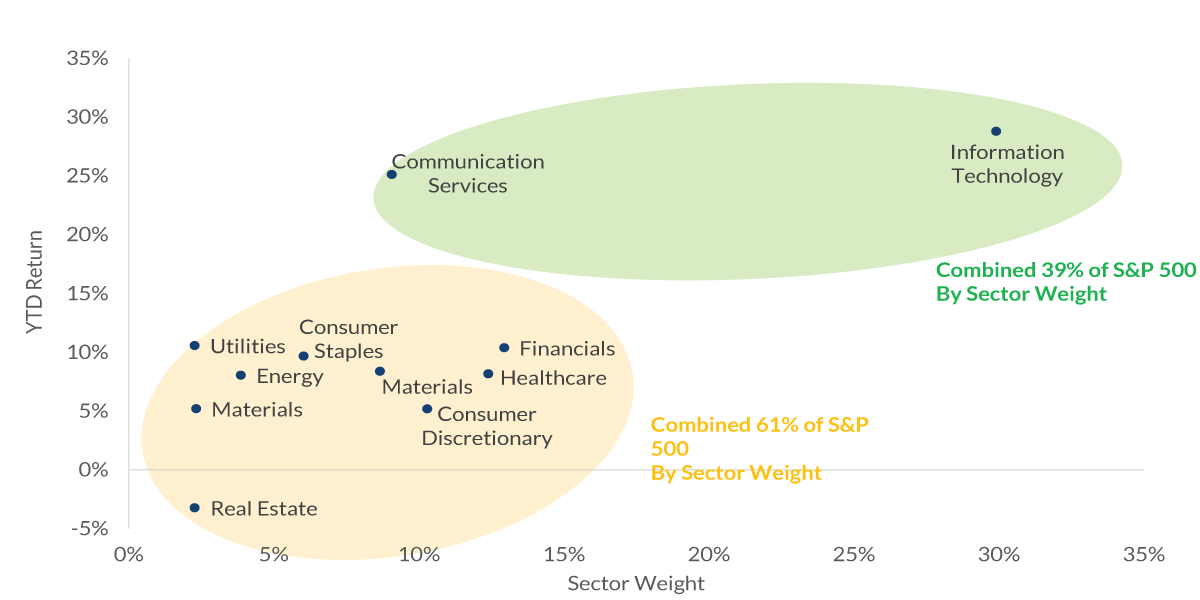

The S&P 500 finished the first half of 2024 near record highs and up 15.3%. While the advance has continued to be driven by growth stocks, especially tech-related, more sectors are participating in the rally this year, delivering solid to strong returns overall year to date. Given high valuations, the Core Equity strategy remains balanced and continues to favor secular growth and high-quality companies, which exhibit above-average margins, earnings growth, and return on invested capital.

Chart 1: YTD S&P 500 Return vs Sector Weight

Source: FactSet, as of June 2024.

Information is subject to change and is not a guarantee of future results.

In Q2, Core Equity returned 4.93%, 65 bps ahead of S&P 500, net of fees. Healthcare, Consumer Staples, and Industrial sectors led performance. Within Healthcare, we prefer biotech pharmaceutical companies over healthcare service providers, as we see greater financial benefits from drug development and fewer policy risks. Companies with exposure to weight loss, cancer, chronic pain, and gene therapy drugs make up the majority of our exposure. In Consumer Staples, two of the companies we own won additional market share by being the price leaders in the industry. EDLP (everyday low price) has gained popularity, as low-end consumers struggle with inflation and high borrowing costs. In the Industrials sector, companies leveraging the benefits of AI, particularly within the data center, electricity, and HVAC businesses, had strong performance.

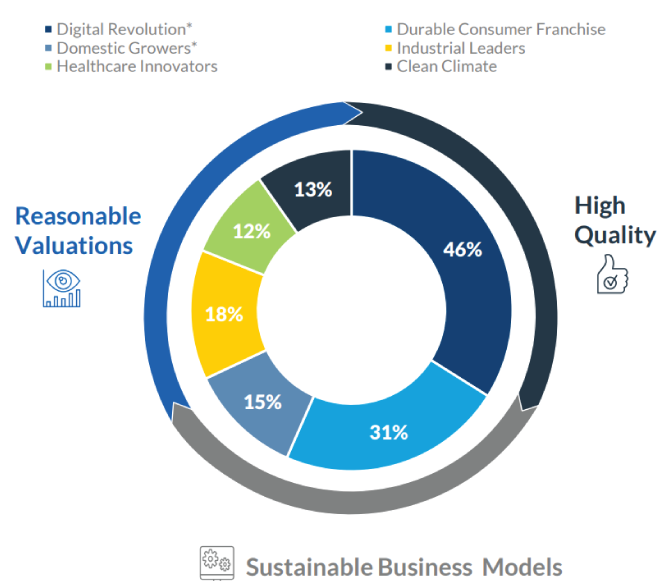

Using quantitative and fundamental research, the Core Equity portfolio is structured by layering quality and valuation metrics over long-term secular themes of Digital Revolution, Durable Consumer Franchises, Healthcare Innovators, Domestic Growers, Industrial Leaders, and Clean Climate, while minimizing risk. During Q2, portfolio tracking error fell from 2.4% to 2.2%, and positioning continued to shift toward the AI mega trend with increases in semiconductor, hyperscale cloud operator, and digital media platforms, and reductions in traditional industries like cable networks, cellular carrier, and payment companies.

Chart 2: Thematic Research Focus

Source: CNR Research, as of July 2024.

*Some stocks are included in more than one theme. Information is subject to change.

Important Information

The views expressed represent the opinions of City National Rochdale, LLC (CNR) which are subject to change and are not intended as a forecast or guarantee of future results. Stated information is provided for informational purposes only, and should not be perceived as personalized investment, financial, legal or tax advice or a recommendation for any security. It is derived from proprietary and non-proprietary sources which have not been independently verified for accuracy or completeness. While CNR believes the information to be accurate and reliable, we do not claim or have responsibility for its completeness, accuracy, or reliability. Statements of future expectations,estimates, projections, and other forward-looking statements are based on available information and management’s view as of the time of these statements. Accordingly, such statements are inherently speculative as they are based on assumptions which may involve known and unknown risks and uncertainties. Actual results, performance or events may differ materially from those expressed or implied in such statements.

Investing involves risk including loss of principal. The market price of a security may move up and down, sometimes rapidly and unpredictably. The securities of mid-cap companies may have greater price volatility and less liquidity than the securities of larger capitalized companies. Larger, more established companies may be unable to attain the high growth rates of successful, smaller companies during periods of economic expansion. Current and future holdings are subject to risk. There is no guarantee the fund will achieve its stated objective.

City National Rochdale, LLC is an SEC-registered investment adviser and wholly-owned subsidiary of City National Bank. Registration as an investment adviser does not imply any level of skill or expertise. City National Bank is a subsidiary of the Royal Bank of Canada. City National Bank provides investment management services through its subadvisory relationship with City National Rochdale. Brokerage services are provided through City National Securities, Inc., a wholly-owned subsidiary of City National Bank and Member FINRA/SIPC.

Index Definitions

S&P 500 Index: The S&P 500 Index, or Standard & Poor’s 500 Index, is a market-capitalization-weighted index of 500 leading publicly traded companies in the US It is not an exact list of the top 500 US companies by market cap because there are other criteria that the index includes.

S&P 500 Growth: The S&P 500 Growth Index is a stock index administered by Standard & Poor’s-Dow Jones Indices. As its name suggests, the purpose of the index is to serve as a proxy for growth companies included in the S&P 500.

S&P 500 Value: The term S&P 500 Pure Value Index refers to a score-weighted index developed by Standard and Poor’s (S&P). The index uses what it calls a “style-attractiveness-weighting scheme” and only consists of stocks within the S&P 500 Index that exhibit strong value characteristics. The index was launched in 2005 and consists of 120 constituents, the majority of which are financial services companies.

S&P 500 Equal Weight: The S&P 500® Equal Weight Index (EWI) is the equal-weight version of the widely-used S&P 500. The index includes the same constituents as the capitalization weighted S&P 500, but each company in the S&P 500 EWI is allocated a fixed weight - or 0.2% of the index total at each quarterly rebalance.

DJDVP: The Dow Jones U.S. Select Dividend Index aims to represent the U.S.’s leading stocks by dividend yield.

Bloomberg Municipal Bond Index: The Bloomberg US Municipal Bond Index measures the performance of investment grade, US dollar-denominated, long-term tax-exempt bonds.

Bloomberg Municipal High Yield Bond Index: The Bloomberg Municipal High Yield Bond Index measures the performance of non-investment grade, US dollar-denominated, and non-rated, tax-exempt bonds.

Bloomberg Investment Grade Index: The Bloomberg US Investment Grade Corporate Bond Index measures the performance of investment grade, corporate, fixed-rate bonds with maturities of one year or more.

The Nasdaq Composite Index is a market capitalization-weighted index of more than 2,500 stocks listed on the Nasdaq stock exchange.

The Russell 2000 Index is a stock market index that measures the performance of the 2,000 smaller companies included in the Russell 3000 Index.

The Bloomberg Magnificent 7 Total Return Index is an equal-dollar weighted equity benchmark consisting of a fixed basket of 7 widely-traded companies classified in the United States and representing the Communications, Consumer Discretionary and Technology sectors as defined by Bloomberg Industry Classification System (BICS).

Definitions

Yield to Worst (YTW) is the lower of the yield to maturity or the yield to call. It is essentially the lowest potential rate of return for a bond, excluding delinquency or default.

P/E Ratio: The price-to-earnings ratio (P/E ratio) is the ratio for valuing a company that measures its current share price relative to its earnings per share (EPS).

The 4P analysis is a proprietary framework for global equity allocation. Country rankings are derived from a subjective metrics system that combines the economic data for such countries with other factors including fiscal policies, demographics, innovative growth and corporate growth. These rankings are subjective and may be derived from data that contain inherent limitations. MSCI Emerging Markets Asia Index is a free float-adjusted market capitalization index that is designed to measure equity market performance in the Asian emerging markets.

City National Rochdale Proprietary Quality Ranking formula: 40% Dupont Quality (return on equity adjusted by debt levels), 15% Earnings Stability (volatility of earnings), 15% Revenue Stability (volatility of revenue), 15% Cash Earnings Quality (cash flow vs. net income of company) 15% Balance Sheet Quality (fundamental strength of balance sheet).

*Source: City National Rochdale proprietary ranking system utilizing MSCI and FactSet data. **Rank is a percentile ranking approach whereby 100 is the highest possible score and 1 is the lowest. The City National Rochdale Core compares the weighted average holdings of the strategy to the companies in the S&P 500 on a sector basis. As of September 30, 2022. City National Rochdale proprietary ranking system utilizing MSCI and FactSet data.

© 2024 City National Bank. All rights reserved.

Non-deposit investment Products are: • not FDIC insured • not Bank guaranteed • may lose value

Stay Informed.

Get our Insights delivered straight to your inbox.

More from the Quarterly Update

Put our insights to work for you.

If you have a client with more than $1 million in investable assets and want to find out about the benefits of our intelligently personalized portfolio management, speak with an investment consultant near you today.

If you’re a high-net-worth client who's interested in adding an experienced investment manager to your financial team, learn more about working with us here.